The congestion on the Bitcoin network is leading to a veritable boom in earnings for those who mine.

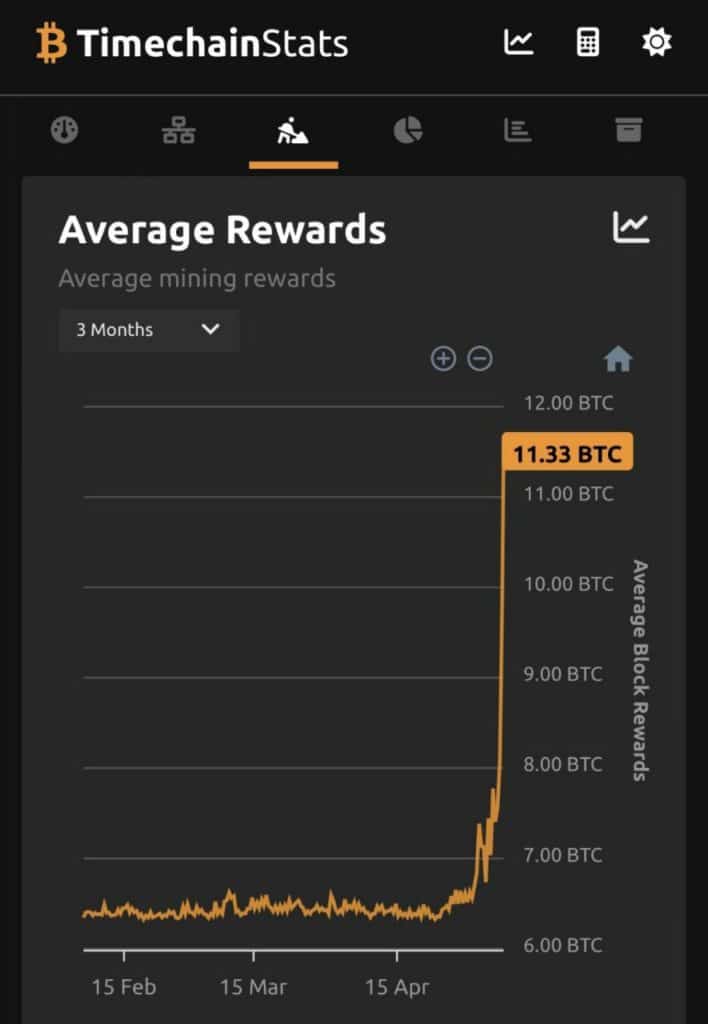

In fact, according to TimeChainStats data, miners cashed in an average of almost 11.2 BTC for every single block mined yesterday.

Suffice it to say that by 1 May this figure was just over 6.5, of which 6.25 was due to the premium that the protocol gives miners by creating exactly 6.25 new BTCs with each block.

On 22 April, the average revenue per block was 6.35 BTC, or just 0.1 BTC more than the premium.

How do miners make money?

Miners have two different sources of revenue.

The first is the premium, i.e. the 6.25 BTC that the protocol currently allows them to create out of thin air with each block.

The second is the fees that each user pays when they want to send their bitcoins to someone else.

The two sources are added together and it is then possible to calculate the total average revenue per block. Of this, 6.25 BTC will always be the premium, while the others are the fees.

It is worth noting that the premium is halved every four years or so, so in the spring of next year it will be increased to 3.125 BTC.

Fees: the silver lining for bitcoin mining operators

It is therefore clear that the boom in miners’ revenues at this stage is solely and exclusively due to the particularly high fees.

Suffice it to say that on 24 April, the value of total fees paid in a single day was more than $13 million, but yesterday it shot up to more than $423 million.

On the other hand, if in April there were rarely more than 400,000 transactions per day recorded on the Bitcoin blockchain, on 1 May there were 682,000, the highest ever, and in the last two days they have remained above 575,000.

The fact is that a block is only mined every 10 minutes or so, and each block can only physically hold a certain number of transactions, as it has a maximum capacity of 1MB.

Right now, for example, there are 423,000 unconfirmed transactions in the Bitcoin mempool waiting to be placed in a block, and it will likely take at least 24 hours for this queue to be exhausted.

However, there is a way to jump this queue, i.e. to get priority from the miners: raise the fees.

In fact, it is the miners who decide which transactions to include in the block they are trying to mine, and they will obviously choose those that allow them to make the most money.

So when the network is congested, as it is these days, fees inevitably rise under pressure from users themselves who want to speed up their transactions.

The current revenue from bitcoin mining

After mid-April, when the average total revenue per block was around 6.4 BTC, the miner who managed to mine a block took home around $174,000 per block mined.

Yesterday, with an average take of 11.2 BTC per block, that figure jumped to $312,000. Approximately 144 blocks are being mined per day.

The really interesting thing is that the cost of mining has not increased.

This is basically a function of the hashrate, which has been around 340 EH/s since March. It is true that there was a peak of over 390 EH/s on 1 May, but this is not much higher than the average for the last period.

Moreover, on the 5th of May it even dropped below 300 EH/s, so mining costs are actually relatively stable during this period.

All of this means that bitcoin miners are actually making a lot of money at the moment, so much so that they have the luxury of not selling much of the BTC they mint in the hope of perhaps being able to resell it at a better price in the future.

Despite this, the price of Bitcoin has been falling since yesterday, but this is most likely due to other reasons.

The cause of the shortage

So why has the number of transactions recorded on the bitcoin blockchain in a single day recently reached an all-time high?

The problem lies with Ordinals, the bitcoin inscriptions that are the equivalent of NFTs on Ethereum.

While normal BTC transactions can be made off-chain thanks to the Lightning Network (LN), ordinals must be registered and exchanged on-chain.

In other words, while BTC transactions may not need to be on-chain to avoid excessive fees, this is not yet possible for inscriptions.

The recent boom in minting and trading of inscriptions is behind the explosion in the number of transactions queuing up on the bitcoin mempool.

The solution, of course, is to use LN for all transactions that do not necessarily require registration on the blockchain.

Suffice it to say that not only does an on-chain transaction currently take a long time to be placed on a block and thus validated, but it also requires a payment of over $31 in BTC to be validated within a few blocks.

On the other hand, by going through LN rather than the blockchain, transactions are instantaneous and fees are only a few thousandths of a dollar.

What’s more, LN cannot really be overloaded at the moment, because with over 18,000 active nodes it can already handle a very large number of transactions without any problems.

{kind=link}